New consumer Duty – Empowering Consumers: Unveiling the Latest Consumer Duty Policy by the FCA

July 2023

Introduction:

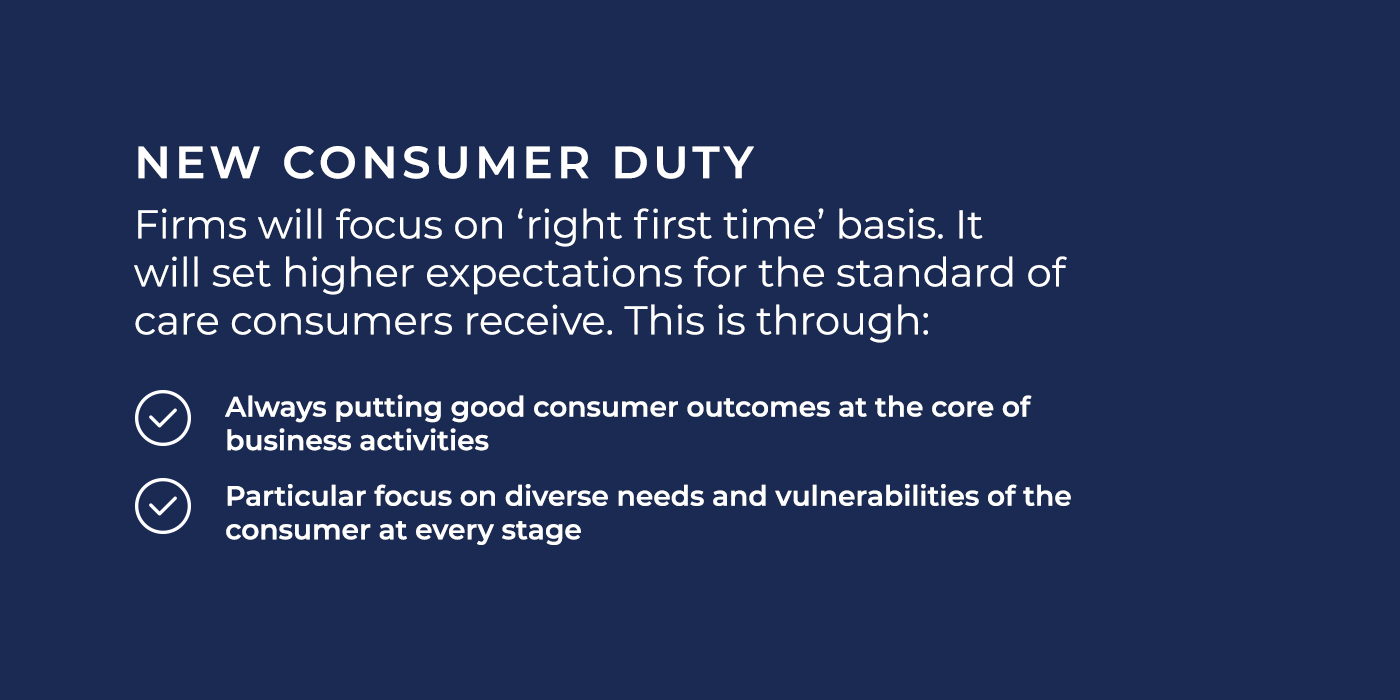

In a constant effort to protect and empower consumers in the financial sector, the Financial

Conduct Authority (FCA) has introduced its latest policy initiative—the Consumer Duty. With a

core objective to ensure fair treatment of customers, this new policy is set to revolutionise the

relationship between financial firms and their customers. With the new rules coming into

force on 31st July, in this blog post, we will delve into the details of the Consumer Duty policy,

exploring its significance, key components, and potential impact on consumers in the UK.

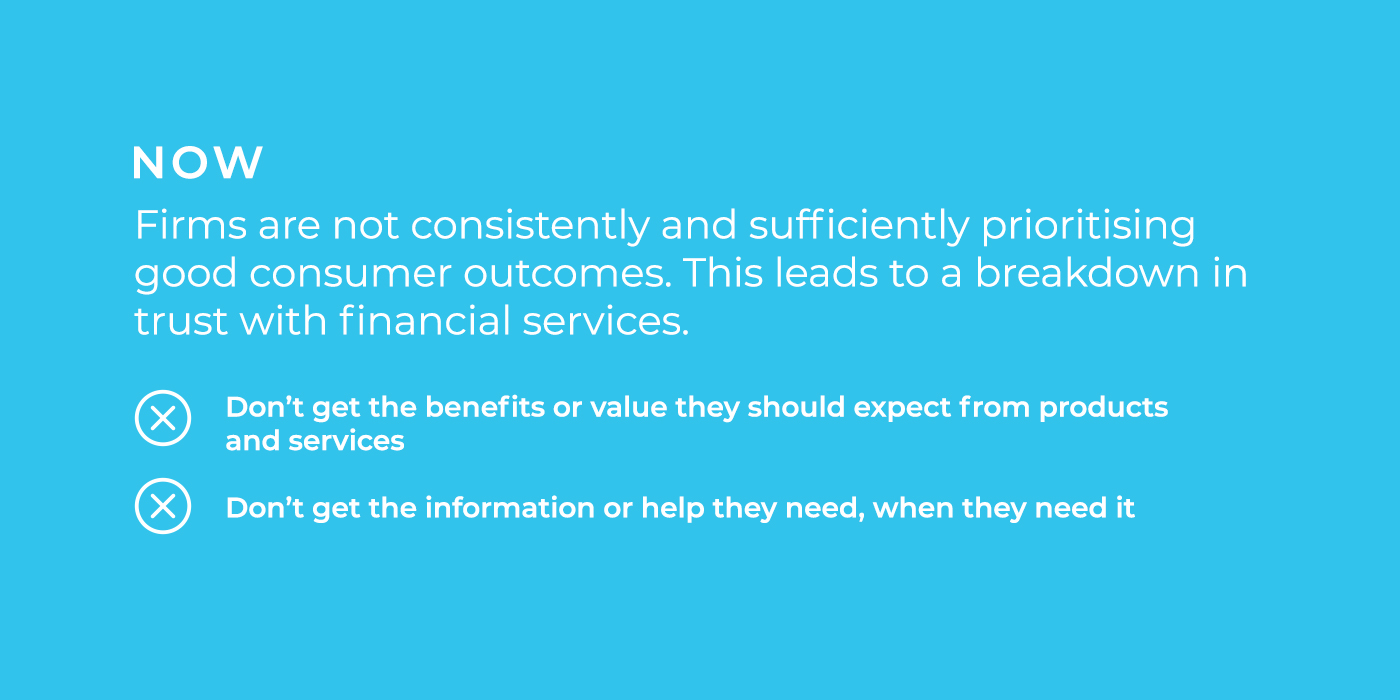

Enhancing Consumer Protection:

The FCA has always placed consumer protection at the heart of its regulatory framework. The

Consumer Duty policy serves as an extension of this commitment, aiming to enhance the

existing conduct rules for financial firms and promote better outcomes for customers. It seeks

to establish a higher standard of care and responsibility in the industry, ultimately empowering

consumers and fostering trust in financial products and services.

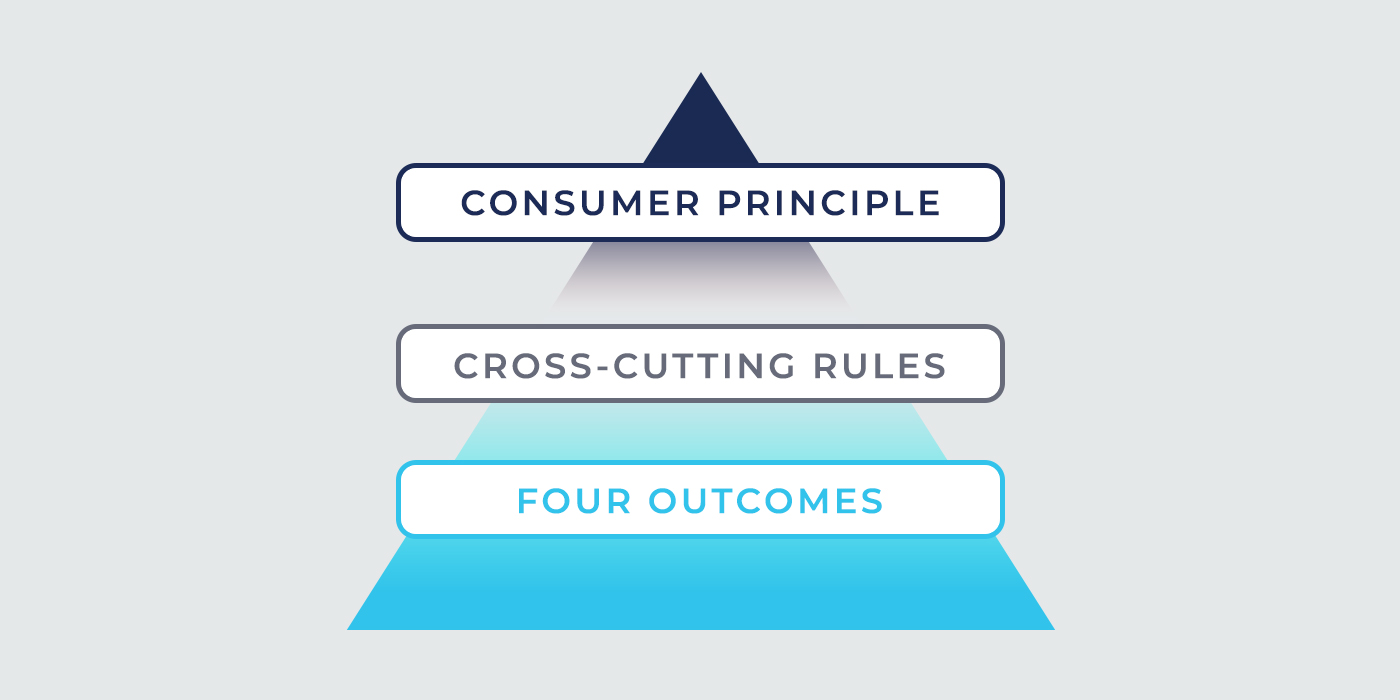

Key Components of the Consumer Duty Policy:

- Duty of Care: The FCA has introduced a formal duty of care for all financial firms. This duty

requires firms to act in the best interests of their customers, to exercise due skill, care, and

diligence, and to take reasonable steps in order to avoid any potential harm to consumers. - Product and Service Quality: Financial firms are obligated to ensure that the products and

services they offer are suitable for customers’ needs and to deliver expected outcomes. Firms

need to focus on maintaining high standards of quality and providing clear and transparent

information to help consumers make informed decisions. - Fair and Accessible Pricing: The Consumer Duty policy emphasizes the importance of fair

pricing for financial products and services. Firms are required to ensure that pricing is

transparent, competitive, and easily understandable. This component aims to tackle issues

such as hidden fees and unfair practices, ultimately promoting a more equitable marketplace. - Communications and Disclosure: Recognising the significance of clear and understandable

communication, the FCA has established guidelines which ensure firms communicate with

consumers in a way that is clear, fair, and not misleading. This component seeks to address

the issue of complex jargon and convoluted terms and conditions, allowing consumers to

make informed decisions without confusion or undue pressure.

Impact on Consumers:

The implementation of the Consumer Duty policy holds significant implications for consumers

across the UK. With the introduction of a formal duty of care, consumers can expect financial

firms to prioritise their best interests and work towards building long-term relationships based

on trust. The emphasis on product and service quality, fair pricing, and clear communication

will empower consumers to make well-informed financial decisions, fostering a more

competitive and customer-centric marketplace.

Moreover, the Consumer Duty policy encourages consumers to actively engage with financial

firms, voice their concerns, and hold them accountable for their actions. The FCA aims to

make it easier for consumers to seek appropriate redress and ensure they have access to

effective dispute resolution mechanisms when necessary.

Conclusion:

The FCA’s Consumer Duty policy is a bold step towards enhancing consumer protection and

promoting fair treatment within the financial industry. By imposing a formal duty of care and

focusing on product quality, fair pricing, and transparent communication, the policy strives to

empower consumers and strengthen their confidence in financial firms. As the UK continues

to foster a consumer-centric financial landscape, this policy is a significant milestone in

safeguarding the interests of individuals and promoting a culture of trust and accountability

within the industry.

With the new rules coming into force on 31st July firms should be on track to meet the

regulators expectations. If you would like to learn more or see how we can help support

you with your ongoing compliance needs then simply complete our contact form and we’ll

get back to you without delay.